The USDC settlement shift

Renting a home has historically been a friction-heavy process. Tenants wait days for ACH transfers to clear, property managers chase bounced checks, and third-party payment processors charge steep convenience fees. The move toward USDC isn't just about adopting new technology; it is a structural fix for a broken payment rail. By settling in a stablecoin pegged to the US dollar, landlords and tenants bypass the traditional banking system's delays, moving money with the speed of the internet rather than the speed of the Federal Reserve's batch processing.

The primary driver for this shift is the elimination of settlement risk. When a tenant pays via traditional methods, the landlord faces the uncertainty of insufficient funds or the multi-day hold period that ties up capital. USDC transactions are final within seconds. This immediacy allows property managers to reconcile accounts in real-time, reducing administrative overhead and eliminating the need for manual reconciliation of pending transactions. For tenants, it means their payment is confirmed instantly, removing the anxiety of "did my rent go through?"

Cost efficiency is equally critical. Traditional bank transfers and credit card payments for rent often involve fees ranging from 2% to 3%, which can add hundreds of dollars to a monthly expense. USDC transactions, particularly on efficient layer-2 networks or stablecoin-native rails, cost fractions of a cent. While the USDC price remains anchored to the dollar, the savings come from the elimination of intermediary fees. This makes USDC not just a technological alternative, but a financially superior instrument for recurring, high-volume payments like rent.

Infrastructure for landlords

Accepting USDC for rent requires a different operational setup than traditional wire transfers or ACH payments. The core challenge isn't the blockchain transaction itself—which settles in seconds—but the bridge between the digital asset and your fiat bank account. To accept USDC effectively, you need a payment processor that handles the compliance layer (KYC/AML) and provides immediate fiat settlement.

Most landlords should avoid holding USDC directly in a self-custodial wallet for rental income. Instead, integrate with a regulated crypto payment gateway. These services act as the intermediary: the tenant sends USDC from their wallet or exchange, the processor instantly converts it to USD (or holds it if you prefer stablecoin revenue), and deposits the fiat into your existing bank account. This approach eliminates the volatility risk and the regulatory burden of managing crypto assets on your own balance sheet.

Compliance is non-negotiable. Under current FinCEN guidelines and state-level money transmitter laws, any entity facilitating the exchange of virtual currencies for fiat currency is considered a Money Services Business (MSB). By using a licensed processor, you transfer the KYC (Know Your Customer) and AML (Anti-Money Laundering) verification responsibilities to them. They verify the tenant’s identity and screen for illicit funds before the transaction completes, protecting your property from being associated with money laundering activities.

The technical infrastructure is minimal on your end. You simply need to generate a unique payment link or address for each tenant’s monthly rent. The processor handles the blockchain monitoring, ensuring the transaction is confirmed on-chain before triggering the fiat settlement. This creates a seamless experience where the tenant pays in crypto, but you receive standard USD in your bank account, ready to cover your mortgage or expenses.

To understand the market context for stablecoin liquidity, which underpins the reliability of these settlements, you can observe the trading volume and stability of USDC against the dollar.

How tenants pay rent with USDC

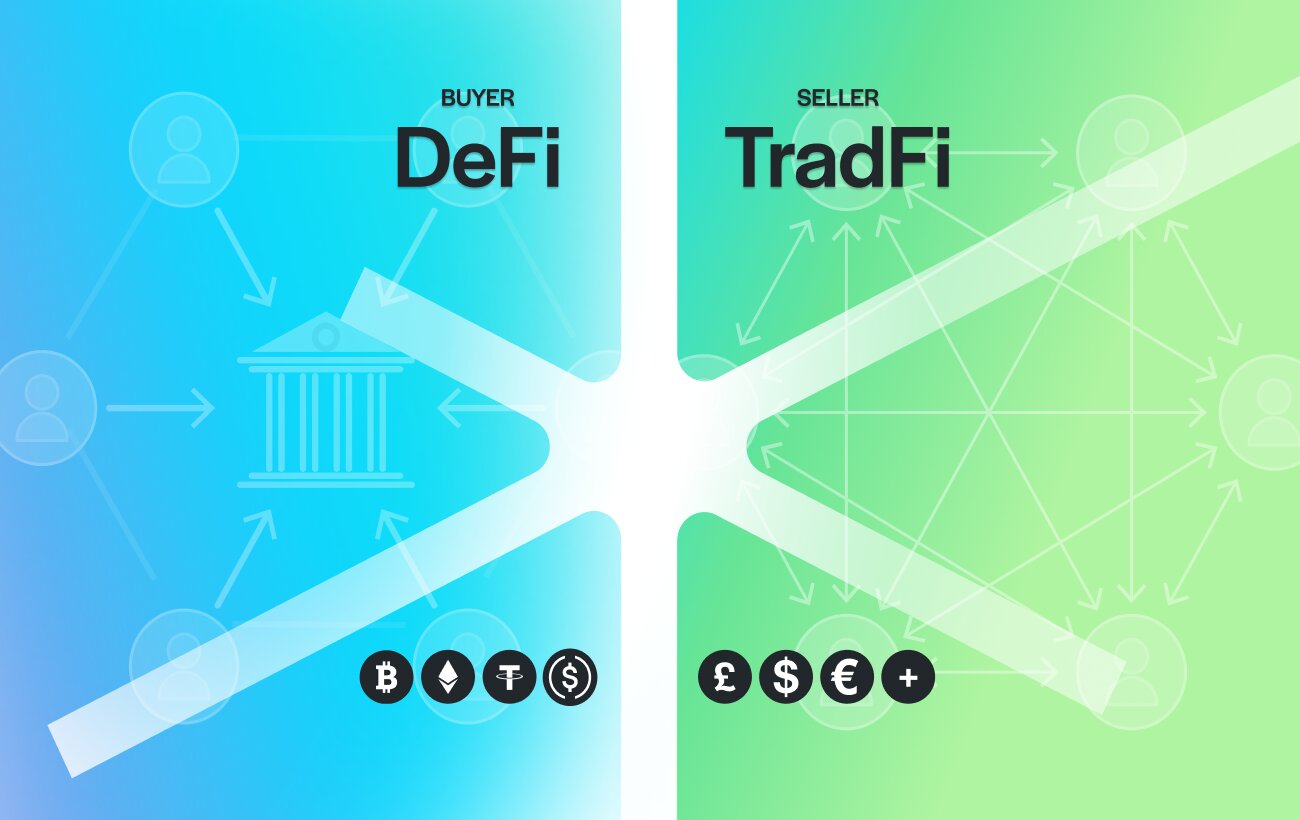

Paying rent in USDC usually happens through one of two distinct pathways. The first is a direct peer-to-peer transfer where you send stablecoins from your own wallet to the landlord’s address. The second is a card-based settlement where a payment processor converts your crypto into fiat currency on the backend. Both methods bypass traditional ACH delays, but they operate on completely different infrastructure.

Direct on-chain transfers

If your landlord accepts crypto directly, you initiate a transfer from your self-custody wallet (like MetaMask or Coinbase Wallet) to their provided wallet address. This is a standard ERC-20 token transfer on the Ethereum network or a Layer 2 solution like Base or Arbitrum. You must ensure you have enough native gas tokens (ETH, ETH on Base, etc.) to cover the transaction fee. The transaction is final and irreversible once confirmed on-chain, so verifying the recipient’s address is the most critical step.

Card-based settlements

Alternatively, you can use a crypto-backed debit card or a dedicated payment processor like Tazapay or Plutus. In this workflow, you load USDC onto the card or app, and the provider automatically converts it to USD at the point of sale or when paying the landlord’s invoice. This method offers the familiarity of a traditional bank transaction and often includes fraud protection, but it may involve conversion fees or monthly subscription costs. Some users report zero fees for USDC transactions on certain cards, while others face standard interchange fees.

Choosing the right method

The choice depends on your landlord’s setup and your comfort with self-custody. Direct transfers are faster and often cheaper if you use a low-fee Layer 2 network. Card-based settlements are more accessible for landlords who only accept traditional bank transfers, as the processor handles the fiat conversion. Always check with your landlord before initiating any payment to confirm which method they support and whether they cover any associated transaction fees.

Adoption Rates and Market Trends

The gap between crypto-native tenants and traditional landlords remains the primary friction point in the USDC rental market. While adoption is growing, it is heavily skewed toward users who already understand self-custody and stablecoin mechanics. For the average renter, the complexity of bridging crypto assets to a fiat-based landlord still feels like a hurdle rather than a convenience.

This divide is largely driven by cost and speed. Traditional bank transfers are slow and often carry hidden fees for cross-border or international payments. In contrast, USDC offers near-instant settlement with predictable, low transaction costs. A tenant using USDC avoids the typical 2.5% processing fees associated with credit card payments or traditional crypto debit cards, making it a significantly cheaper option for both parties when infrastructure is in place.

To understand the practical differences, compare the core mechanics of USDC rent payments against traditional bank transfers:

| Feature | USDC Rent | Traditional Bank Transfer |

|---|---|---|

| Settlement Speed | Seconds to minutes | 1-3 business days |

| Cross-Border Fees | Near zero (network gas) | High (wire fees, FX spreads) |

| Accessibility | Requires crypto wallet | Universal (bank account) |

| Transparency | Public ledger traceable | Private bank records |

Infrastructure providers like Circle and Reap are working to bridge this gap by automating the conversion and compliance layers. However, until landlord-facing tools become as seamless as Venmo or Zelle, USDC adoption will remain niche, driven by efficiency seekers rather than the mass market.

Essential tools and platforms

To pay rent with USDC, you need three things: a secure wallet, a payment processor that settles to fiat, and a reliable way to move funds. The infrastructure has matured significantly since 2024, but the stack still requires careful selection to avoid high fees or settlement delays.

Start with a self-custody wallet like MetaMask or Rabby. These are your gateways. For actual rent payments, use a dedicated crypto-to-fiat gateway such as TrustLinq or BitPay. These services handle the conversion and deposit directly into your landlord’s bank account, removing the volatility risk from the transaction. Always verify that the landlord accepts the specific settlement method before initiating the transfer.

Security is non-negotiable. Since you are moving significant value, hardware wallets are the standard. They keep your private keys offline, protecting your USDC from phishing and malware. The following hardware options are the industry standard for secure storage.

As an Amazon Associate, we may earn from qualifying purchases.

Common rental payment: what to check next

Paying rent with USDC removes the friction of traditional banking rails, but it requires a shift in how you view affordability and communication. Most tenants worry about hidden fees or landlord skepticism, yet the mechanics are straightforward when you stick to established infrastructure.

What is the 2% rule in rentals?

The 2% rule is a shortcut investors use to gauge if a property will generate strong cash flow. It suggests your monthly rent should be at least 2% of the property's total purchase price. For example, a $200,000 home should rent for $4,000 monthly to meet this benchmark. While this helps investors, tenants can use it to spot undervalued markets where USDC adoption might be growing faster due to lower transaction costs.

How much should my rent be if I make $3,000 a month?

Financial planners generally recommend spending no more than 30% of your gross income on rent. If you earn $3,000 monthly, your rent should ideally stay at or below $900. Using USDC doesn't change this fundamental ratio, but it does eliminate the 2.5% processing fees often charged by credit cards or third-party payment apps, effectively giving you more disposable income within that same budget.

What should I avoid saying to my landlord?

Never tell a landlord you "lost your job" or "can't pay" without a concrete plan. These phrases trigger alarm bells about risk and instability. Instead, frame the conversation around infrastructure: explain that you are switching to USDC for faster, fee-free settlement. If you anticipate a delay, propose a specific date for the transfer rather than offering vague excuses. Trust is built on transparency and reliable settlement times, not just the currency used.

No comments yet. Be the first to share your thoughts!